By Debra R. Richardson, MBA, CFE, CAPP

In today’s fast-paced business environment, the integrity and security of financial transactions are paramount. Organizations are increasingly exposed to the risk of fraudulent activities, in particular vendor payment fraud.

Our 2024 research shows that finance teams continue to battle against fraud. 88% said their company has fallen victim to some type of fraud, with 17% saying they experience it frequently.

As companies strive to protect their financial assets and ensure seamless payment processes, the method by which vendor remittance details are handled becomes a critical focal point. This article delves into the intricacies of managing these details, highlighting the vulnerabilities associated with in-house processes and presenting outsourcing as a viable solution to mitigate fraud risks.

Risk of Fraudulent Payments With In-House Vendor Payments

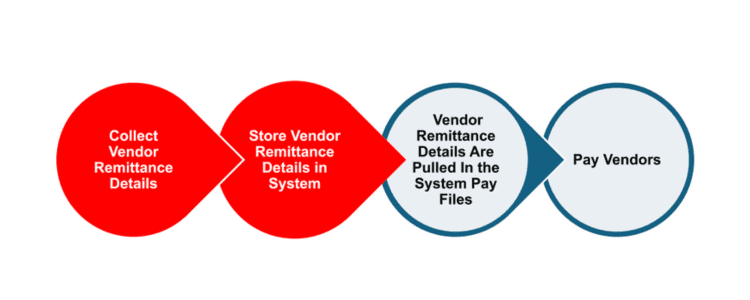

When vendor payments are handled in-house there are a lot of moving pieces, but this is the high level of the collection, storage and use of vendor remittance details.

Flow of In-House Vendor Setup and Payment

- Collect Vendor Remittance Details – Often this process involves collecting vendor remittance details via risky email. Team members collecting this information are expected to immediately recognize red flags of fraud. Accessible validations are performed to ensure the information is accurate, and that the remittance information belongs to the vendor.

- Store Vendor Remittance Details in System – Vendor bank details for electronic payments or the remittance address for check payments are entered into the system.

- Vendor Remittance Details Are Pulled In the System Pay Files – Once pay cycles are run, separate pay files will generate based on payment type and pull in the remittance details from the vendor record to be included on the pay files.

- Pay Vendors – Once the pay cycles are generated and released to be sent to the bank for electronic payments or to have checks printed for check payment method vendors.

The problem with this process is that the collection of vendor remittance details is risky. Furthermore, storing this information in the vendor master file means that there is risk of not only external fraud from requiring team members to collect this information so they can update it when needed, but also from internal team members looking to change the vendor remittance information to their own right before the pay cycle.

So how can these two problems be solved to reduce the risk of vendor payment fraud?

Reduce the Risk: Outsource Vendor Payments

In general, outsourcing your vendor payments means that payment information will be sent to the third-party payment provider who will work with the vendor to identify a payment method, and remit that payment on your company’s behalf.

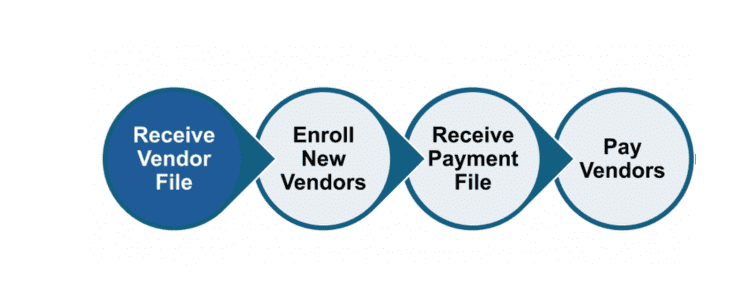

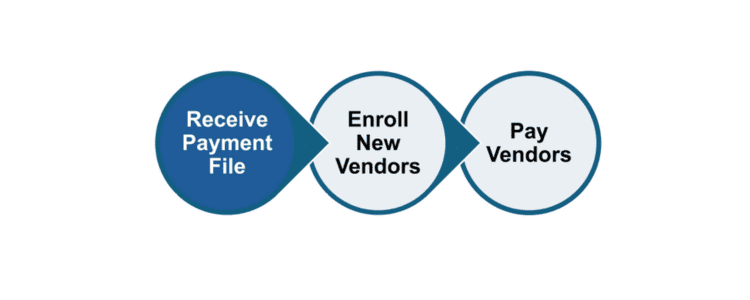

Potential Flow of Vendor Setup and Payment on Third-Party Platform

Four Benefits of Outsourcing Vendor Payments

- Avoid Collecting Vendor Remittance Information – If vendor remittance information does not have to be stored on the vendor record, then that means that the team member does not have to process that remittance details change that came through email. Just forward that email to the third-party payment solution provider to handle.

- Avoid Storing Vendor Remittance Information – When vendor remittance information is not stored in the system there is no chance to expose vendor sensitive information to any team members, who could be social engineered into revealing that information. Also, because pay cycles are no longer being generated, the system is not pulling remittance information that could have been changed by a team member engaging in internal fraud.

- Potential Fraud Liability Coverage – In the event there is a fraudulent payment, depending on the third-party provider and the type of payment method for the vendor, the liability or “risk” payment loss is covered.

- Enhanced Security – Consider the third-party provider as professional in vendor setup and maintenance. Not only do some invest heavily in state-of-the-art security measures to protect against fraud. In the selection process, confirm that their vendor enrollment team is trained in the latest techniques to avoid fraud and that they use advanced encryption techniques, multi-factor authentication, and real-time monitoring to detect and prevent unauthorized transactions.

What Outsourcing Vendor Payments Won’t Do

- Avoid Setup of the Vendor Record – Vendors will still need to have a vendor record, just without the remittance details. Vendor records are still required to generate purchase orders, track payment activity and other tasks in financial operations.

- Decrease Turnaround Time – Outsourcing your vendor payments won’t speed up your vendor setup and on-boarding process, and it may even increase it. Payment providers can have a long turnaround time to enroll new vendors, and especially to change existing vendors. Expect a turnaround time of 10-15 days.

Conclusion

While outsourcing vendor payments offers substantial benefits such as enhanced security, potential fraud liability coverage, and the elimination of the need to collect and store vendor remittance information, it is not without its limitations. Companies must still manage vendor records and may experience delays in vendor setup and onboarding. Ultimately, the choice to outsource should align with the company’s strategic goals, risk tolerance, and operational needs, but can go a long way to reducing the risk of payment fraud inherent when making payments in-house. Third-party providers can differ on the point that they enable a new vendor on their platform. For some, new vendors are enrolled based on being added to the vendor master file, while others may wait until that new vendor is included on a pay file for their first payment.